How big is India's Consumer Market?

Do the recent claims of 30mn-50mn addressable market hold water?

Beszel. Ui Qoma. A murder and an investigation.

China Mievelle in his landmark book The City and The City, tells the story of two cities occupying the same “space” simultaneously, with the residents of each city, wilfully ignoring the other. And in this weird space-time, happens a murder.

Tor.com described The City and the City as "the most awarded book in the history of books" (referring to the history of speculative fiction). Yes, it is that good! And we highly recommend it.

What does “The City and The City” say about our society?

The book is a thinly veiled allegory to how our cities are organized - the poorest, the struggling, and the desperate in the lowest strata, the dreamy and the hardworking above them, and the wealthy at the very top.

It is also the story of your city and mine.

In India, there are three cities living side by side. As Inspector Hathi Ram Choudhury of Paatallok, says -

“Ye jo duniya hai na duniya, ye ek nahi teen duniya hai. Sabse upar swarg lok, jisme devta rehte hain. Beech mein dharti log jisme insaan rehte hai, aur sabse niche paatal lok jaha keede rehte hai.”

“You see, this creation isn’t just one world, but split into three different worlds. At the very top are the heavens, where the gods reside. In the middle, is where we humans live, and in the very bottom, the netherworld, live the maggots and the despicables.

- Inspector Hathi Ram Choudhary, Paatal Lok (2020)

Lay of the Land

Over the course of the next thousand-odd words, we will try to put together how India lives. Specifically, we will construct the income statements of an urban, upwardly mobile, English-speaking, Westernised household; how Middle India lives and dies, saves and spends; and lastly, how do the struggles of Forgotten India translate into hard economics.

Putting these three pictures side by side together, we will draw some startling conclusions regarding the mistakes our home brew startups are making.

The Varied Lives of The Kumars

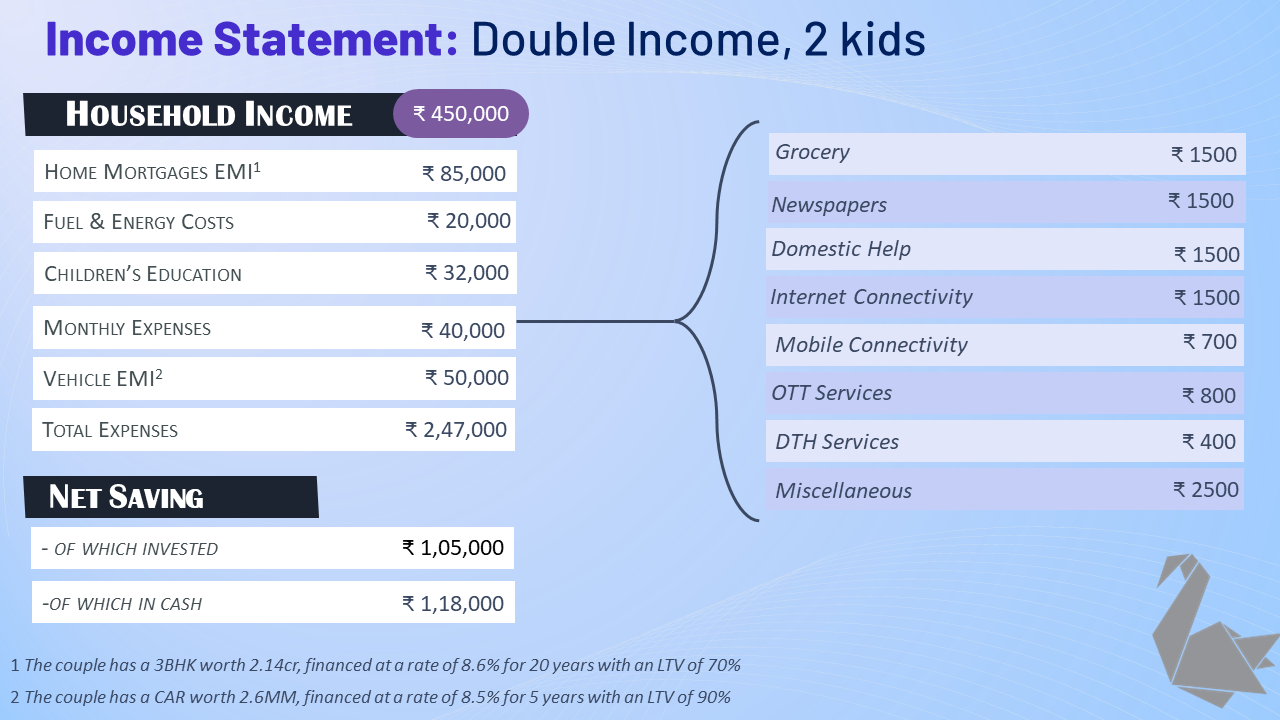

Arun Kumar, 33, along with his wife Richa, 28, constitute one household of the roughly 50mn households in India. They make up the nouveau-rich professional class, hit payday by their PG degrees. Fluent grasp of English, and Westernised tastes, mark their personalities. Usually hailing from Technology, Finance, or Consulting (TFC), they are upwardly mobile, with a household income of >350k INR per month, having 2 vehicles (1 of which is older and paid for), and a mortgage against a flat in the city.

Arun and Richa travel abroad every year, except for those pesky Covid years, and desire novel experiences in each of their trips. So, it is not mere Europe travel, but rather, visiting Iceland for witnessing Aurora Borealis.

Their investment portfolios are mutual funds dominated by a smattering of direct equity investments (which usually perform poorly, owing to their lack of time outside office hours). You, as a reader of this newsletter, are more likely to be part of this cohort, than the ones coming next.

The lifestyle of the “Arun Kumar Household” is very similar to an ex-pat in Singapore or Australia and barring the failures of the State in providing public goods, it is more or less the same.

What does “barring the failures of the State” imply?

The inability of the State to provide high-quality roads, affordable potable tap water, high-quality electricity supply, law, and order, etc.

The Dreams, Ambitions, and Perseverance of Abhilash Nair*

Abhilash Nair, 22, recent graduate from one of the 2000 odd engineering colleges dotting through Indian education landscape. He dreams of earning $11k annually (~900k INR), but only managed to land a job that one-third that.

He is not unhappy though. Plenty of his friends are yet to earn even that much. “Most of my friends, have joined these IT companies. Their in-hand is far lesser than mine”, says Abhilash, referring to the salary a professional in India receives post statutory deductions.

A vast majority of engineers that India churns out every day get hired in the numerous body shops that dot the Indian IT landscape. Infosys, TCS, Wipro, HCL, Mindtree.

Funny thing?

Each of them on average pay the same amount for a fresher and has been paying so since 2007. INR 250,000, annually ($3200/year). Abhilash counts himself lucky for the extra INR 4000 every month.

He struggles with English, has never tied a necktie before (which will be a major cause of panic before his first client meeting, which will happen about a year or two in the job), and plans to get married in the next 5 years. He is 22 and lives with his friends in a PG.

In financial parlance, he is termed a new to credit customer. He will not have a credit card, will not be eligible for a home loan, and the only bank which will grant him a 2-wheeler vehicle loan is the one with which he has a salary account.

He is planning for his own home in the next 7-10 years, which will be a low-income group 1 BHK. But he doesn’t quite know the “path” to reach from “here” to “there”, except for an increase in salary.

So he also plans to raise his skills along the way. For the next 4-5 years except for Edu-tech, no other signs of conspicuous consumption will be visible in his income statement. An avid consumer of YouTube, his leisure is spent equally split between Youtube and games on his mobile.

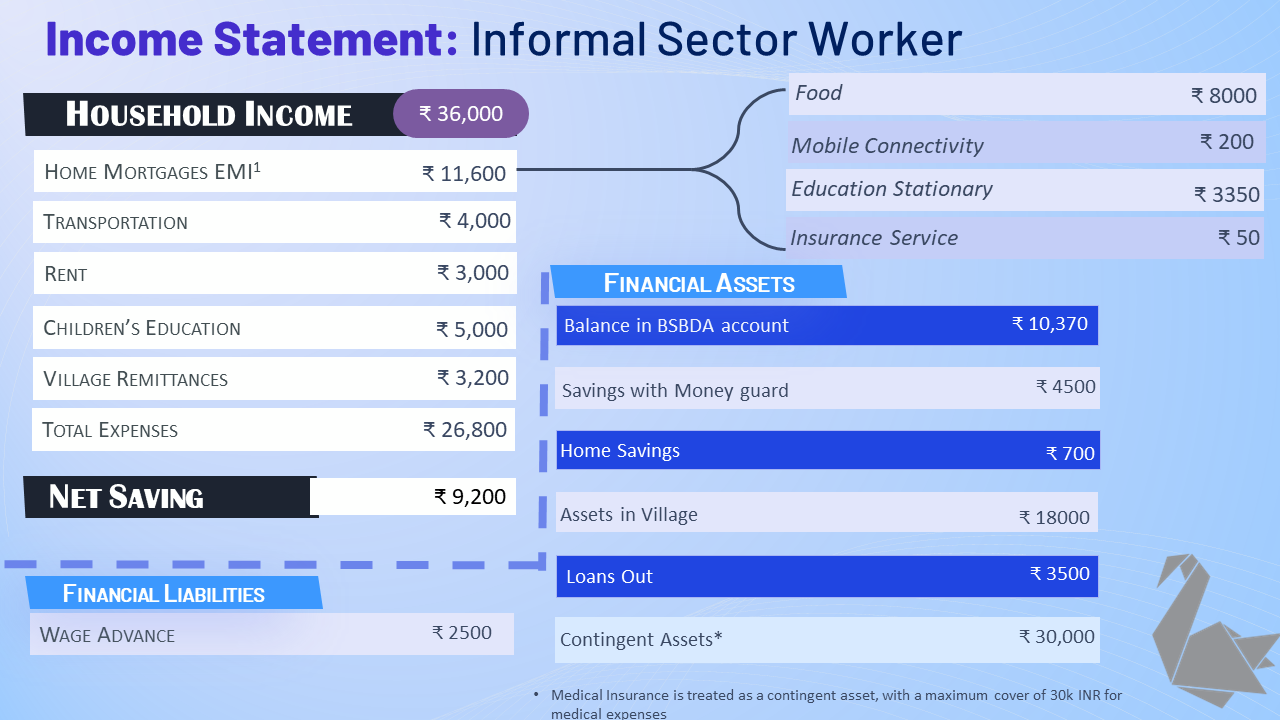

The Relentless Life of Bacchu Singh

Bacchu Singh, 32 lives with his wife, Muniya, and two kids in a slum of East Delhi. Bacchu Singh, a 10th pass from a Tier III town of North India works two jobs to earn a monthly income of INR 36,000, slightly more than what Abhilash Nair earns every month.

He wakes up at 6.00 am every morning, and rushes to work at a local car wash in Noida, where he works from 8 to 6 everyday. He tends to 10-15 cars a day and earns INR 15000 ($190) a month. He rushes to catch the 6.30pm metro from Noida Sector 143 to East Delhi. He takes his dinner, spends some time with his family, and sets out a bit before midnight to the DMRC train depot, where his second job starts just after midnight. He is part of a 10 men cleaning crew of 4 trains. There are 5 such teams working every night, cleaning the 20 trains that ply on East Delhi lines.

While the work is expected to take about 5 hours, he manages to wrap it in 2 hours. Quiz him, and he replies with a tinge of pride “Phast kaam karte hain, bahut time se jo kar rahein hain”. I work fast, been doing this for quite some time. Press on a bit more, and he sheepishly smiles and admits, “The Supervisor is not finicky”. He earns INR 15000 per month from this job.

“I am a fast worker, been doing this for quite some time”

Muniya, Bacchu’s wife works as a maid for 4 homes in a nearby gated society. Together, she brings $75 per month (INR 6000). Bacchu Singh has a smartphone, watches Hindi news uploaded on Youtube, and dreams of getting his two kids educated in an English medium school.

Very little to go in the form of fixed assets, Bacchu has a BSBDA account with the local private bank. He has a debit card, sure - but no credit card. He is deemed too risky by the bankers and will be never given a home loan, vehicle loan, or a personal loan.

Bacchu saves diligently and lends to neighbors, not to earn interest, but to earn goodwill and a “social insurance” during economic stresses. It rankles Bachhu for having to lend money to neighbors, and picking up the “credit risk”, but he has little choice, in a fast deteriorating informal economy marred by economic uncertainty.

Following is his income statement and balance sheet:

Singh also sends about INR 1200 every month to his village in Giridih, Jharkhand - where his nephew is holding onto this amount and is on the lookout for a calf/cow that will act as an investment. In his own words if they are able to purchase a cow - “…to badhiya rahega”. It will be a good investment.

Currently, his nephew is holding INR 18k, while a good quality breed of cow will easily cost 85k-100k INR. Bacchu is woefully short. He is also banking on the agreement his family has with the local farm owner. Work in exchange for money and fodder.

Singh, opened a BSBDA account sometime in 2018, and has been trying to squirrel away whatever is possible, whenever is possible. It’s a different matter, that almost every 6-9 months, Singh faces uncertainty (economic or health, which draws down on his savings).

Muniya, in her wisdom, has also lent to a neighborhood self-organized women’s group - which “guards the money” on behalf of Bacchu and Muniya. Lending money to the moneyguards serves as a signaling mechanism* that Bachhu and Muniya “trust” the slum community and here for a longer run. This “trust” serves as a “collateral” in which they dip for an emergency line of credit, whenever the Singh family needs it - especially in times of overnight emergency.

Life of Bacchu Singh and Muniya is filled with daily low-grade anxiety, around living conditions, inflation, health facilities, and employment stability. They are afraid to lend to the local community, but it is a tacit “cost of living”. They intuitively understand the credit profile of the local neighborhood group is not really “AAA”, and they manage their credit exposure by lending a small amount compared to their overall capability.

The 3 Indias and seductive lure of eCommerce

“Ye jo duniya hai na duniya, ye ek nahi teen duniya hai.

“You see, this creation isn’t just one world, but split in three.

- Inspector Hathi Ram Choudhary, Paatal Lok (2020)

The story of these three households is the story of India and ensconced in it, is the story of Indian e-commerce. The success and the failures, the joys and the disappointments, the up-rounds and the down-rounds.

Market Sizing

The Top 10%: The Great India, The Rich India

We estimate about 100MM adults in the creme de la creme of society. With a resource of about $2.5tn under their control, the bulk of their spending is experience-oriented, novelty-seeking, and exotic in quality. As a result, they would rather ‘value’ a gift of a Gucci bag, than a mass-market bag that is widely available on Amazon. They would gravitate towards, an up-market, status-signaling Apple Watch than no-watches.

As a result, while their consumption appetite is big, little if any translates to online mass-market shopping, which in turn prevents the eCommerce players from effectively performing “wallet mining”.

The Consuming 10%: The Middle India

Sandwiched between the urban rich, and urban poor- are the upwardly mobile, freshly graduated engineer in Tier 1 cities, middle-income families in Tier 2 -3 cities, and everything in between. This layer is about 100MM strong, but commands only $500bn in resources annually.

And this is the most valuable layer for the eCommerce layer. It is this layer that is the most active consumer of Youtube videos, and it is this layer that spends spent the most time on TikTok. It is this layer, which is the driver behind the white consumer goods revolution a few years back, and it is this layer that economists are singing praises of.

Their way to climb up is ‘Exit’ - exit from India for higher education abroad.

The Poorest 50%: The Forgotten India

The desperados, the mas pobres , the lost, the hungry, and the strugglers - spread across rural and urban India, constitute the poorest 50%.

This 50% live in urban villages across the cities of India, and rural villages across the countryside.

They are the ones who live in slums, and they are the ones who suffer the brunt of archaic ideas like caste. To calculate GDP, income, and consumption for them will be a slap on the cheeks of any upright Indian. So we won’t. So poor are they, that economists don’t measure their income, they measure their “deprivation”.

For them, the only way to climb up claw their way up is ‘Education’ and ‘English’.

Needless to say, short of Youtube consumption in vernacular languages, they aren’t really setting the cash registers ringing for the D2C players.

So what’s the TAM really?

WealthTech: $50Mn revenue TAM

The target market of WealthTech is Category #1, but unfortunately, this group will rather opt for high-touch Premier Banking Services of HSBCs of the world, but not a run-of-the-mill mutual fund management app.

At a 1% commission rate, they will be commanding access to an AUM of $5bn, which is pushing it. So good luck, WealthTech!

Personal FinTech: $2.5bn revenue TAM

We estimate only the top 20% of Middle India, and the bottom 5% of Professional India will adopt a credit card payment solution, personal expense management app, and/or those fancy saving solutions that use sweep accounts integrated with expense solutions.

We estimate it to be a total of 25MM customers, willing to shell upto $100 annually on subscribing to these apps.

Premium OTT: $7.5bn revenue TAM

At 50Mn high-value households willing to shell up to $150 annually (1000INR/month, 80INR/$) for quality content, the TAM stagnates at $7.5bn.

OTT players like Netflix have barely been able to touch $190Mn revenue from India. That really explains 2 things:

That, a company with the marketing budget and content engine of Netflix is barely able to break past $200mn revenue implies, how small the serviceable operating market must be.

There is only room for 2 premium OTT players in India.

This 1+1 breakup is visible across many premium services [Uber and Ola, Swiggy and Zomato, IPL and EPL]

Mass Market OTT: $5bn revenue TAM

Mass Market OTT is the only space that cuts through the economic lines and will be the real beneficiary of cheap 5G internet. Along with the middle category, the top category of consumers will also purchase subscriptions to mass-market OTTs (along with a premium OTT subscription).

As mobile internet penetration in India picks up, rural India will start taking subscriptions as well (this is an aggressive assumption, since rural India doesn’t like digital transactions).

We estimate 250Mn customers with an annual entertainment budget of $20.

eCommerce: $12bn revenue TAM

We estimate the 100mn strong Middle India, to power eCommerce businesses. The average annual spend will hover around $120 (INR 10,000 annually), thus turning the TAM to around $12bn.

Is it any surprise that short of Amazon and Flipkart, there has not been a third player in the running? If TAM is $12bn, a SOM is most likely to be $3bn, split between the two, and no place for a third wheel.

Conclusion

The phenomenon of 1+1 is playing out fair and square everywhere in India. Premium consumer services like Licious have been only able to serve 1MM households to date. Repeat customers will be far less. That, the number of luxury consumption startups are yet to scale properly is a testament to the fact that there is a stark difference between the investor pitchbooks and the line manager handbooks.

Nitin Kamath has been prescient when he said India’s fintech userbase is merely 150MM strong. Our numbers bear out.

Having delved deep into the Indian consumption class, allow us to circle back and revisit the story of Beszel and Ui Qoma. The murder of the young woman, which serves as the premise of the novel, was also a symbolic murder of our own humanity. That lady, turned out to be the resident of a third hidden city, residing in the interstices of the two cities. That, is the city of the desperados and the mas pobres, the desperates and the stagglers. The city that we knowingly steer clear of.

Look at the consumption pyramid above.

While the “Great India” is spoilt for choices, the Forgotten India is begging for some. While the “Great India” is looking westward for inspiration, the Forgotten India is looking sideways for survival.

Beszel and Ui Qoma is amongst us. Our startups need to innovate not for themselves, but on behalf of the Forgotten India.

Very well written!

The groceries amount for the first category seems incorrect...else great read