If Old Banks are Pink Elephants, can Neo Banks fly?

If Old Banks are Pink Elephants, can Neo Banks fly?

Everyone is writing the Old Banks off. But are Neo Banks ready to pick up the mantle?

The painting ‘The Money Changer and His Wife’, by Quentin Matsys hangs in the famous halls of The Louvre. Done in 1514, the work showcases a middle age banker.

It is proof of the resilience of banking as an industry, that sitting half a millennia later we still ‘get’ the concept of moneylending.

Banking has been around the block for quite a while and it has adapted remarkably with changing technology paradigms…but, only till now.

The rise of neobanks threatens banking as we know it. Banking, for all it deals with and stands for, is a very tangible business. We see the neighbourhood branches, bankers, appraisers and forms.

Oh lord! the endless reams of KYC forms!

If technologists have their way, shoot the banking industry in its heart with a silver bullet, drive a stake and smash its head for good measure.

But can they really?

The Seductive Promise of NeoBanks

NuBank goes vertical

On 9th of December 2021, shares of NuBank, the Brazilian fintech/neobank (during the course of the article, we will be using ‘fintech’ and ‘neobank’ interchangeably) listed on Nasdaq and immediately rallied 15%, valuing the company at a mouthwatering $45billion.

That is a lot of money. Enough to make its 39 year old co-founder, Cristina Junqueira, a billionaire.

And if it was ever a question, NuBank has an annual run rate of $132million, in red. Yes, it is losing money hand over fist.

But lets talk about value proposition.

The Unbundling and Re-bundling of Traditional Businesses

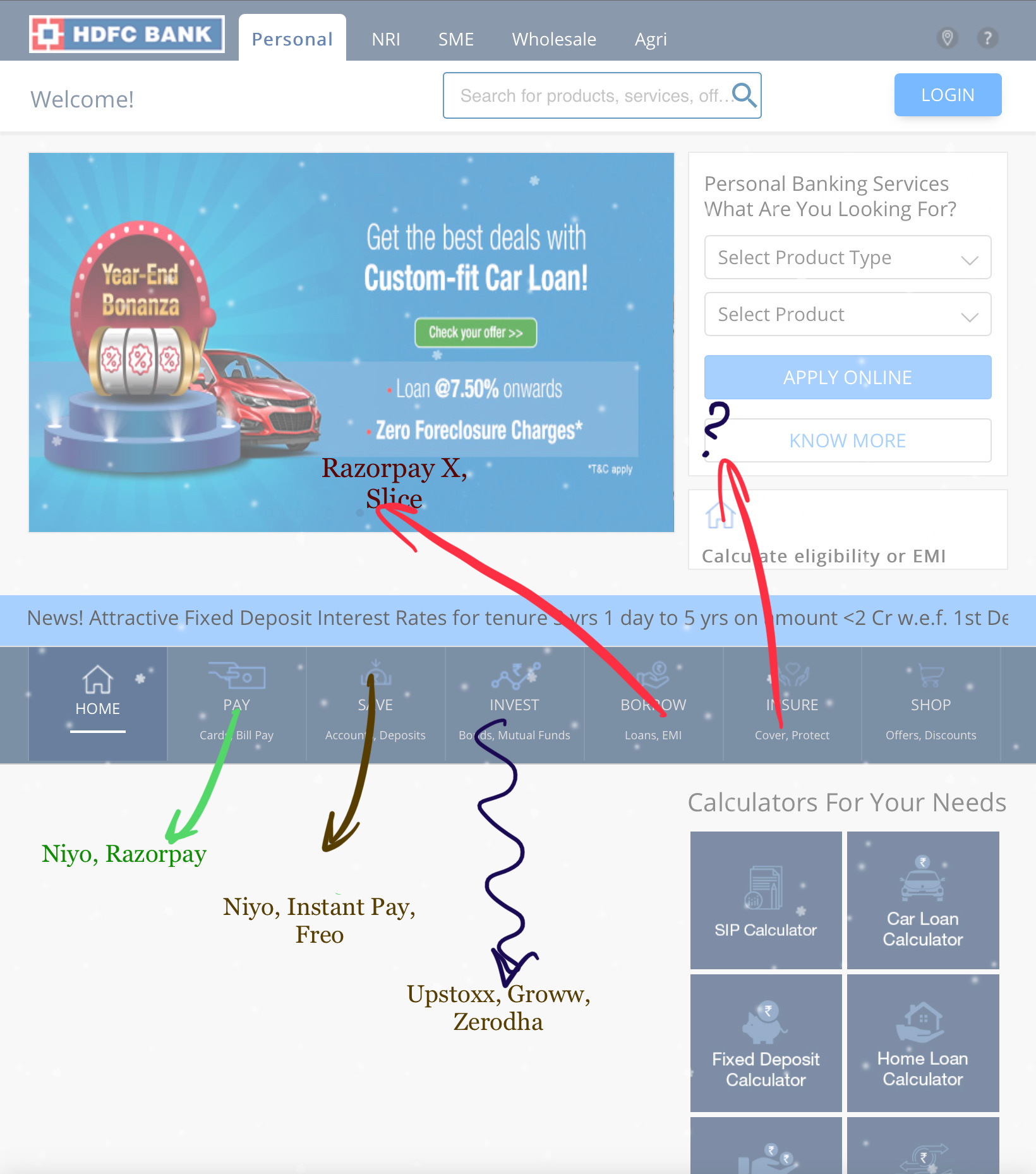

Take a long, careful look at the home page of HDFC Bank.

HDFC has split its value offerings across 6 major verticals: PAY (credit cards, bill payments etc.), SAVE (accounts, deposits), BORROW (loans, EMI), INVEST (bonds, mutual funds), INSURE (cover, protection) and SHOP (offers, discounts).

The new innovation Buy-Now-Pay-Later, on which we did a cover story last week: unbundles the “BORROW” and “SHOP” verticals bundles them together, into one product.

The game plan is easy: unbundle and re-bundle.

Unbundling and Re-bundling of Banking Ops

What a neobank proposes is a fundamental redesign of the banking experience. The promise of neo-bank holds even more allure, as legacy banks (esp. in West), groan under the curse of legacy systems. (1,2,3).

The unbundling of operations into front-office, middle-office and back-office (a favorite of western banks), is at risk.

Neo-banks aim to re-bundle it all up and put it together with a nice sash of technology and offer to the modern customer in ultra-sleek UX.

Neobank’s Tryst with Destiny

Neobanks, marketed sexily as ‘challenger banks’ emerged after the 2007-09 crisis.

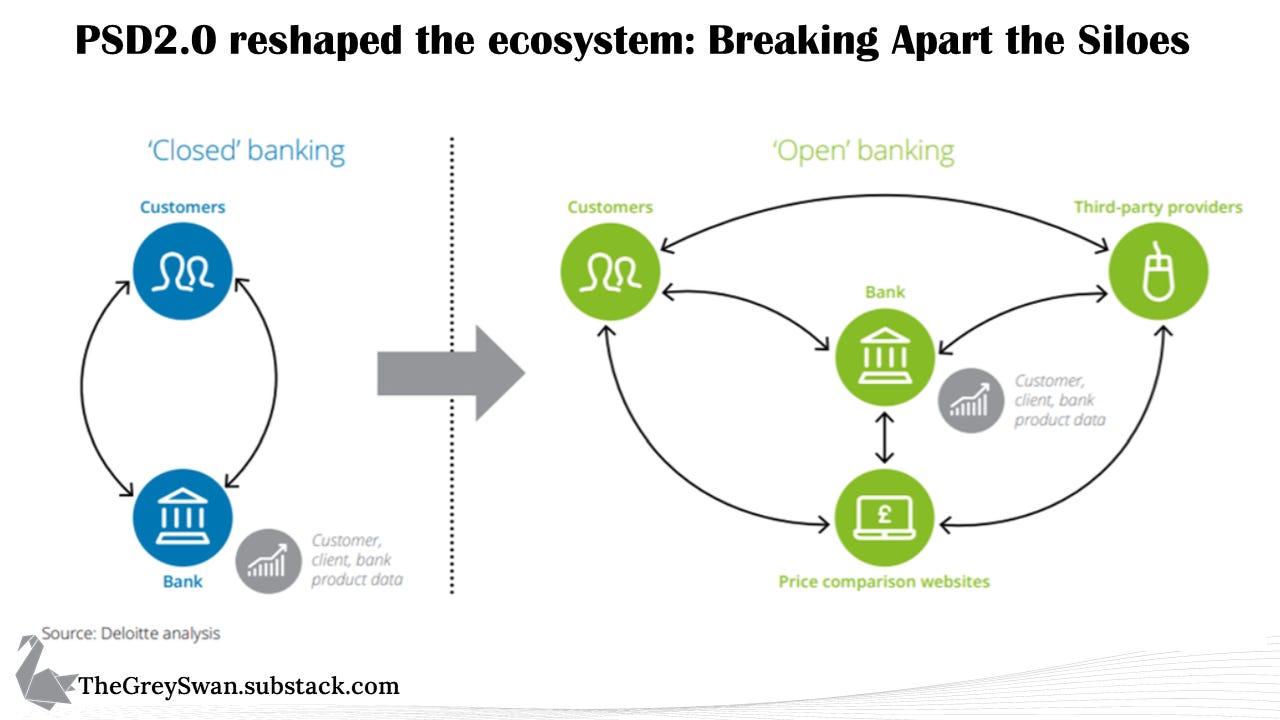

But what really drove this innovation, was the pincer attack on the incumbents. A pincer-attack led by customers on one flank and regulators at the other.

After the global financial crisis, the incumbents lost their pole position when it came to evoking trust in the minds of their customers. Regulators, on the other hand, wanted banks to loosen their grip. So they drove the stake into the heart of Big Banks, by issuing Payments Services Directive(PSD). The directive forced the Big Banks to become more transparent and provide easier access to new market entrants.

The neo-banks bolstered by the opening up of the ecosystem, the data and the services - managed to shake the ground from under the Old Banks.

The age of neo-banks had begun.

N26, a Germany based neobank acquired 7MM customers in the 8 years since its operation. Its USP? A client onboarding process that takes no more than 8 minutes.

Its valuation? $9billion.

Something else was happening in another continent - South America. If European banks were hobbled by low trust and regulatory scrutiny, Brazilian banks took a chrysknife knife and drove it through their own heart.

Brazilian banks like Itau, Caixa, Banco do Brasil acted and behaved much like monopolists- atrocious customer care, poor or no innovation in financial products, completely divorced from the needs of the masses, were their hallmarks.

Co-founder of NuBank, Cristina Junqueira -the billionaire we introduced a couple of scrolls back, handled the credit card division for Itau. “I never really got why we had to shove these horrible products down people's throats. Customers hated it” she was quoted by Forbes.

No wonder, NuBank trades at an eye popping valuation of $45billion. The number of customers, it services? 48million.

Hard Numbers

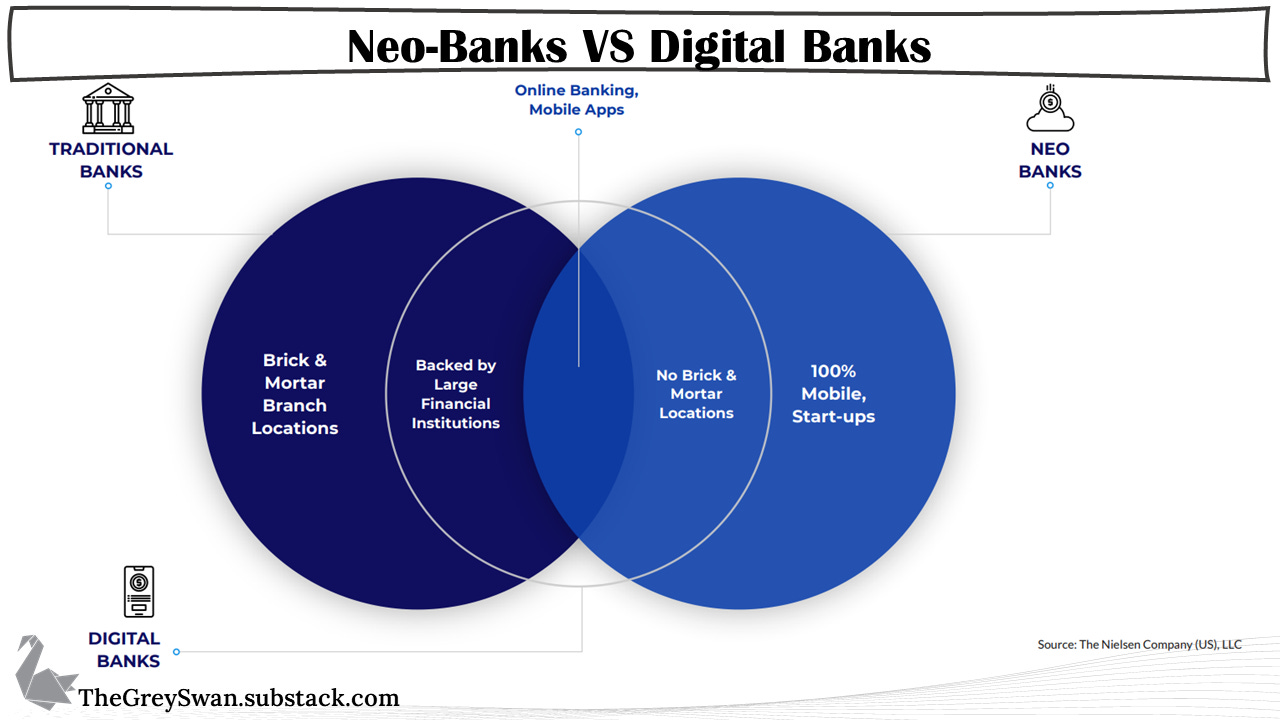

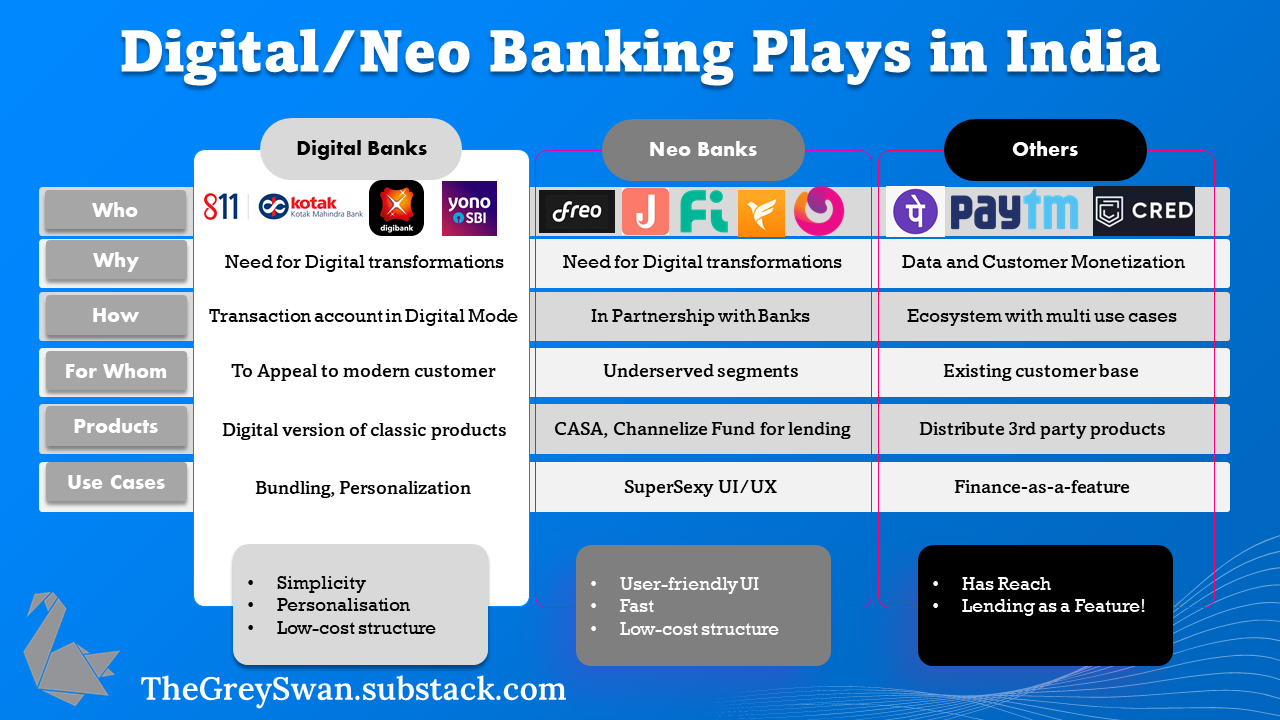

The term neobank does not convey much. The term digital bank isnt helpful either. Let’s peel the layers apart.

A neobank can be a standalone bank in itself, much like the original neobank of the US - “The Bank of Internet” was founded in 1999, it is currently known as Axos bank. Such neobanks have a full banking license and operate on their own…or, alternatively, a neobank can be a front-end focused operation only. Thus acquiring customers for a partner bank.

Roughly, full-stack neobanks across geographies are valued at $1000 per customer. In contrast, valuation of front-end focussed neobanks can vary widely.

For instance, Step - a banking app targeted at teenagers, raised $100MM in April this year in Series C funding, right after it signed 1.5MM customers. Poor estimation, but about $100 of incremental invested capital per customer.

Square, Jack Dorsey’s other startup, positioned itself fair and square (pun intended) in the domain of small and medium businesses. Today, it is trying to set up a new digital bank from scratch- with all the bells and whistles.

Its valuation? $110billion. Active users? 36MM. The reason for such numbers? Its a B2B neobank.

A Cold Splash of Water: Setting up an Indian Square

Neobanks seem very sexy. But take a cold hard look, and one finds few winners where the ‘financial intermediation layer’ is alive, dynamic and innovative. And that is especially true in India’s case.

Let us perform a thought experiment. Let us try to copy the playbook of Square in India. Dorsey’s Square solved payments first. So lets try doing it in India. But wait, India has already solved its payments problems. UPI provides instant cash transfer, NEFT and RTGS settlement runs 24x7, payment is not a layer that causes pain, but eases it.

How about turning into an alternate lending?

India has always been a credit hungry country. So this idea has potential. Yet, we don’t have our own equivalent of Payment Services Directive(remember the European law, that started it all?) to break apart the data and services.

As a result, the underwriting standards of these ‘alternate lenders’ are uniformly atrocious. So the fintechs, strike a Faustian bargain: ‘Growth. Underwriting be damned’.

In their playbooks, the only way to build high-quality consumer data is by customer acquisition.

A Cold Splash of Water Part II: A rundown of Indian neo-banks

The promise of neo-banks has always been alluring and intuitive. Digital technologies, customer delight, kick-ass UX. What can be simpler than that?

Much to their surprise, Indian fintechs are finding themselves to be glorified customer acquisition app.

Here’s how it works. Indian neobanks need to partner with an OldBank to conduct their operations. For example Niyo has partnered up with Equitas, DCB and few others.

The key pitch to customers is a 7% savings account. In a country, where savings rate hovers at 2-4%,this is big! The resulting deposits are transferred to the ‘Old Banks’, which serves to shore up their CASA.

So who really is the bigger winner here?

Obviously the ‘Old Banks’. Their market valuations are intrinsically linked with the cost of their funds and shoring up CASA is the easiest way to lower this cost, and get some love from public market investors.

The only way fintechs, like Freo, Instant Pay and Razorpay X can make money is by lending. So they enter into an agreement with their partner banks to be offered a line of credit of up to 80% of the mobilized savings at a facility fee of 3%.

In turn, the fintechs lend to their customers at 18-20%. They pocket 15-18% of the spread, after paying the facility fee. Which is lucrative, right?

Wrong! The fintechs have been atrocious in their lending standards and their cost of lending is a big hurdle to their growth.

On top of that, these ‘neo-banks’ are always put on constant notice, as their partner banks can sever the ties anytime. As Niyo quickly discovered when IDFC First severed its ties in mid-2021.

This dependence is not seen elsewhere. And herein, is the rub and a case-study for “Wholesale Transfer Pricing”.

Wholesale Transfer Pricing: Neo-Banks on the receiving end?

Wholesale Transfer Pricing(WTP) is a term coined by John Malone, the famous CEO of Liberty Media. In short, WTP occurs when a player, already in a business relationship with another, is held hostage by the latter.

Think about, a bad business marriage gone abusive, with no possibility of divorce.

A real life example is when Disney cut its normal service to YouTube TV, in the middle of Lakers vs Timberwolves game. If interested to know more, one can read this post. To know more about WTP, 25iq has a brilliant post

Coming to the curious case of fintechs and the partner banks, consider this: the partner banks are in no way dependent upon the neo-banks, but, the neo-banks are. Completely dependent.

As a result, the partner banks exert a disproportionate effect on the fintechs.

The consequence?

The partner banks can jack up the prices, discontinue their services and anything in between, overnight.

This ‘inter-locking’ of relationship is much stronger in the case of co-branded cards, non-fungible assets like Demat accounts etc.

Through the Looking Glass: The Perspective of the Indian Banks

So what US banks wanted to do but couldn’t, Indian banks planned and achieved

If startups made ‘growth at any price’ dogma into a fad, then Indian banks ensured it becomes a fashion.

Indian banks are hungry to ride this golden period of banking, where others do the hard work for them. Federal Bank, a traditional bank, liaisons with 50+ fintechs, across the entire stack of banking services.

Gold Loan? Check! (rupeek)

EMI on checkout? Check! (PayU)

Full stack for Neo-Banks? Check (Jupiter, epifi and DGV are customers)

Crypto/Remittances? Check, Check, Check (Ripple, R3)

Spanning across 300+ APIs, 13 API bundles, Federal Bank sits at the center of it all.

To underline the extent of the success, Federal Bank in May 2021, announced a staggering 70% growth in gold loans. Any guesses how?

Ding, ding, ding! That’s right, Rupeek it was.

In fact, as late as last month, Rupeek has made fresh loans of 300crores. Its only anybody’s guess, how much will Rupeek get to keep it.

While, Federal Bank is the glowing example of an Indian banking system which has found its mojo back, it is not the only one.

V.V. Balaji, CTO of ICICI Bank in the 14th Mint Annual Banking Conclave said something prescient - ‘we will be there wherever technology takes us’.

This confidence stems from a happy accident. Indian banks never had the burden of history hobbling its growth. So what, US banks wanted to do but couldn’t , Indian banks planned and achieved.

‘Advantage Indian banks has compared to many of the peer banks in developed countries, is that we don’t have too much of legacy and mainframes…’, says Balaji.

So lets take a stock of the situation. Indian fintechs are overly dependent upon ‘Old Banks’ who have the chops to navigate the technology waters, and the lending landscape, and the regulatory compliance . Phew!

Slice and dice it any way, Indian fintechs risk becoming the pansy on the poker table.

Round and Round Goes the Wheel of Fortune

If this was not clear till now, we at Gray Swan are not hyped up about the future of neo-banks. We see it as just another ‘style’ of losing money, that is hip these days.

Put in simple words, the entire unit economics of these neo-banks are moving against them, and in favor of the Old Banks. And it will continue to be a movement that is net positive for Old Banks, till VCs continue to incentivize this mad rush of ‘customer acquisition’.

We at The Gray Swan are reminded of the famous bumper sticker joke, that proliferated in US just after the dot com bust. It read - ‘O, Lord, give me just another bubble, this time to make my money back’.

It seems, that the Old Banks are praying similarly - ‘O, Lord, give us another set of dumb competition, to make all our money out of’

Round and round, goes the VCs money, only to land up in the balance sheets of the Old Banks.

Oh the irony!

The Last Words

We started this piece, with Mastys’s famous masterpiece - ‘The Money Changer and His Wife’. Its only fitting that we revisit this masterpiece as we draw an end to this piece.

In the painting, in front of the moneylender, sits a shiny piece of metal, seemingly disconnected from everything around it, serving apparently no purpose.

Zoom close into it, and we will find something interesting. One has to magnify to find the image of a man, sitting by the window painting.

Much like, a subtle picture is hidden in plain sight, the success of Old Banks is staying hidden under the din of noise that neo banks are making.

Make no mistake. If you are a public market investor, you will be well rewarded to cast a positive light on these banks, and a harsh light on the neo-banks that aim to displace them.

Great article Soham! Could you please elaborate on this para a bit more- ''The only way fintechs, like Freo, Instant Pay and Razorpay X can make money is by lending. So they enter into an agreement with their partner banks to be offered a line of credit of up to 80% of the mobilized savings at a facility fee of 3%. In turn, the fintechs lend to their customers at 18-20%. They pocket 15-18% of the spread, after paying the facility fee.''

1) How is the spread 15-18%?

2) What do you mean by mobilized savings, are these the deopsits that are brought in by fintechs for Partner banks?

3) And the line of credit is offered by partner banks for 80% of these deposits fintechs bring in at just 3%?

Could you please state an example for the above? Perhaps some fintech who models its business like this?

Best,

Pankaj