India Branded Pharma: Sales, Share, and Therapy Trends.

Understanding India's Branded Pharma

The pharmaceutical industry’s history is a sprawling tale of innovation, profit, and controversy, tightly linked to scientific breakthroughs, economic shifts, and public health needs. Across cultures, alchemists and monks (Hakims [Arabic for "wise one"] and Vaidyas) played pivotal roles in developing and transmitting knowledge of herbs, compounds, and their applications, often blending spirituality, science, and philosophy. Their work laid the foundation for modern pharmacology, botany, and chemistry.

By 19th Century, the isolation of active compounds like morphine (1804) and quinine (1820) marked the shift from crude remedies to targeted drugs. The discovery of penicillin by Alexander Fleming (1928) transformed medicine. By the 1940s, companies like Eli Lilly scaled production, saving millions during WWII. Some Pharma firms soon grew into global players, driven by R&D investments. The industry’s ability to deliver life-saving drugs cemented its economic power.

Indian Pharmaceutical Market (IPM)

The India is often referred to as the "Pharmacy of the World" due to its large-scale production of generic medicines and low-cost vaccines. While India holds the third rank globally in pharmaceutical production by volume, a substantial portion of its domestic market is driven by branded generic drugs, which constituted approximately 87% of the IPM by value in 2023. The IPM witnessed a Compound Annual Growth Rate (CAGR) of 9.1% between 2019 and 2023 and is projected to grow at a CAGR of 9.6% to reach INR 4,60,000 crores by 2030.

The growth of the IPM is influenced by a combination of factors, including price increases, volume expansion, and the introduction of new products. Notably, in recent years, price growth has been a significant driver of IPM growth. The domestic formulations sector, which heavily features branded generics, has shown resilience despite various market disruptions. Leading domestic pharma companies derive a substantial portion of their revenue, ranging from 20% to 100%, from domestic formulation sales.

Sales and Market Share of Branded Pharma

The Indian domestic branded pharma market is characterised by a mix of Indian and multinational pharmaceutical companies.

It is crucial to note the dominance of generics within the IPM. In 2023, generic drugs constituted approximately 97% of the market by value, with innovator/patented drugs making up the remaining 3%. Within the generics segment, branded generics held the lion's share at around 87%, followed by trade generics at about 10%. This highlights the significance of understanding the dynamics within the branded generics space to comprehend the overall domestic pharma landscape.

Note: MAT (Moving Annual Total) refers to the cumulative sales or turnover of pharmaceutical products over the previous 12 months, calculated on a rolling basis. It provides a snapshot of the market's performance by aggregating data from the most recent 12-month period.

As of MAT (Moving Annual Total) March 2025, Sun Pharma held the top position in the IPM with a 7.9% market share. Other prominent players forming the top five included Abbott, Cipla, Mankind, and Alkem.

Comparison between Domestic and MNC Growth: In March 2025, domestic companies' sales grew by 9.0% YoY, slightly lower than the 10.4% YoY growth achieved by MNC companies.

Growth Leaders in March 2025: JB, Cipla, FDC, Ipca, Glenmark, Pfizer, Himalaya, Sun, Intas, Abbott, Zydus, Corona, and Torrent demonstrated strong YoY sales growth ranging from 10-17%. This suggests positive momentum for these companies in the short term.

Underperformers in March 2025: Conversely, Alembic, Sanofi, Dr Reddy’s, Eris, Indoco, and Macleods experienced lower YoY sales growth in March 2025, ranging from 1-5%.

Key Therapy in Branded Pharma

1. Endocrinology (Anti-diabetic) The anti-diabetic segment is a significant contributor to the IPM, driven by India’s growing diabetic population, estimated at over 100 million in 2024. The segment’s prominence underscores the rising burden of lifestyle diseases in India.

2. Endocrinology (Hormones) is projected to grow at a lucrative rate due to increasing prevalence of endocrine disorders, such as thyroid imbalances and hormonal deficiencies

3. Cardiology is the largest therapy area in the IPM, reflecting the high burden of cardiovascular diseases, which account for over 80% of cardiovascular-related deaths in India. The segment’s dominance is expected to continue due to lifestyle-related risk factors and an aging population.

4. Respiratory is another key growth area, particularly due to worsening air pollution and rising cases of asthma and Chronic obstructive pulmonary disease COPD. It is smaller than cardiology or anti-infectives, but its double-digit growth indicates significant demand, especially in urban areas.

5. Gastrointestinal segment addresses a wide range of digestive health issues, supported by increasing prevalence of metabolic liver diseases and digestive disorders.

6. Anti-Infective segment is driven by the increasing burden of infectious diseases and innovations in antifungals, antimalarials, and antivirals.

7. Pain Management grew by 13% in November 2024, driven by paracetamol-based formulations. The segment benefits from rising demand for both acute and chronic pain relief, with innovations in injectable therapies.

8. Dermatology Subcategories like emollients and sunscreens are key contributors, driven by rising consumer awareness and aesthetic demand. The segment’s growth is bolstered by biologics and branded generics, particularly in urban markets, but specific market size data is unavailable.

9. Neurology segment is driven by rising cases of neurodegenerative disorders and increased prescription rates for chronic conditions.

10. Orthopedics Growth is driven by an aging population and rising cases of osteoporosis and arthritis. Market size is likely smaller than cardiology or anti-infectives.

11. Gynecology therapies are growing due to increasing focus on women’s health, and benefits from rising demand for treatments for PCOS and gestational diabetes.

12. Immunology includes treatments for autoimmune diseases, and is an emerging segment driven by biologics and biosimilars. Growth is supported by increasing R&D investments and demand for specialty drugs.

13. Urology segment’s growth reflects rising demand for men’s health treatments.

Trends and Observations:

Chronic vs. Acute Therapies: Chronic therapies (e.g., Cardiology, Anti-diabetic) consistently outperform acute therapies (e.g., Anti-infective, Pain Management). This trend is attributed to factors like population growth, lifestyle changes, and urbanization.

Chronic therapies experienced a higher growth rate of 11% year-on-year compared to acute therapies at 8% year-on-year in March 2025. Several therapies showed strong year-on-year growth, driving the overall IPM performance. These include urology, cardiac, gastro-intestinal, onco, neuro, VMN (Vitamins, Minerals, and Nutrients), and derma.

Price growth has been a significant driver of IPM growth in recent years, offsetting some deceleration in volume growth, particularly in acute segments.

New product launches, brand building, and strategic M&As are key strategies employed by companies to enhance their market share within specific therapeutic areas. For instance, Mankind's acquisition of Panacea's India business aimed to strengthen its presence in the chronic space.

The increasing adoption of generics, particularly through trade generics and Jan Aushadhi stores, poses a challenge to the growth of branded formulations. We talked about this here.

Company Performance and Key Therapeutic Drivers:

Sun Pharma: Their MAT Mar-25 sales grew by 10.3% year-on-year, with Neuro/CNS and Cardiac being key therapeutic drivers. Their March 2025 sales grew by 12.6% year-on-year.

Abbott: Their MAT Mar-25 sales increased by 9.5% year-on-year, with Anti-diabetic and Gastro-intestinal being significant contributors. Their March 2025 sales grew by 11.0% year-on-year.

Cipla: They recorded a MAT Mar-25 sales growth of 7.4% year-on-year, with Respiratory being a key therapeutic driver. Their March 2025 sales showed a strong growth of 16.3% year-on-year.

Mankind: Their MAT Mar-25 sales grew by 7.5% year-on-year, with Cardiac showing strong growth. Their March 2025 sales grew by 7.8% year-on-year.

Alkem: Their MAT Mar-25 sales grew by 5.9% year-on-year, with Anti-infectives being a major therapy. Their March 2025 sales grew by 8.1% year-on-year.

Lupin: Their MAT Mar-25 sales grew by 7.8% year-on-year, with Cardiac being a significant therapy. Their March 2025 sales grew by 7.3% year-on-year.

Intas: They experienced a strong MAT Mar-25 sales growth of 11.0% year-on-year, driven by Neuro/CNS. Their March 2025 sales grew by 11.6% year-on-year.

Torrent: Their MAT Mar-25 sales grew by 8.4% year-on-year, with Cardiac as a key therapeutic driver. However, their March 2025 sales growth was lower at 3.6% year-on-year.

JB: They showed a significant MAT Mar-25 sales growth of 12.0% year-on-year, with Cardiac and Pain/analgesics as key therapies. Their March 2025 sales grew even higher at 17.1% year-on-year.

Ipca Labs: They recorded a strong MAT Mar-25 sales growth of 13.2% year-on-year, with Pain/analgesics being a primary driver. Their March 2025 sales grew by 14.3% year-on-year.

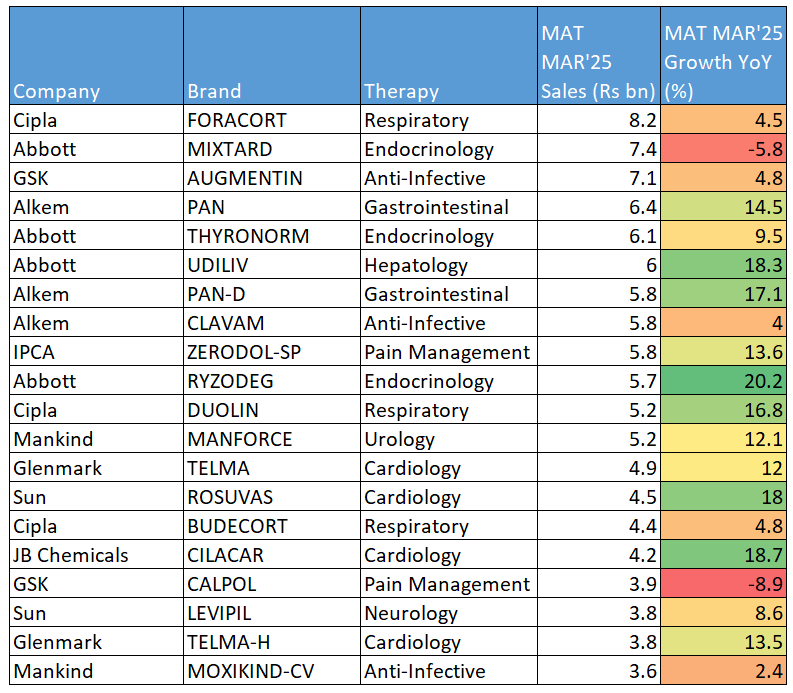

Top Brands in IPM

We picked the List of top 150 Brands across the company and therapy, a quick snapshot of 20 brands is

email us at thebizdomin@gmail.com to get the full list and other data of this post in a excel file.

Now, if we create a pivot of these, we get the Therapy level data as follows

In summary, the branded pharmaceutical market in India is experiencing growth, driven by price increases and new product launches, with volume growth also showing improvement. Chronic therapies are growing faster than acute therapies. Key therapeutic areas like cardiac, neuro/CNS, anti-diabetic, respiratory, and gastro-intestinal appear to be significant drivers for many top companies. However, the increasing adoption of generic medicines through alternative channels is posing a challenge to the volume growth of branded formulations.

Not for Everyone. But maybe for you and your patrons?

Dear GS,

I hope this finds you in a rare pocket of stillness.

We hold deep respect for what you've built—and for how.

We’ve just opened the door to something we’ve been quietly handcrafting for years.

Not for mass markets. Not for scale. But for memory and reflection.

Not designed to perform. Designed to endure.

It’s called The Silent Treasury.

A sanctuary where truth, judgment, and consciousness are kept like firewood—dry, sacred, and meant for long winters.

Where trust, vision, patience, and stewardship are treated as capital—more rare, perhaps, than liquidity itself.

The two inaugural pieces speak to a quiet truth we've long engaged with:

1. Why we quietly crave for signals from rare, niche sanctuaries—especially when judgment must be clear.

2. Why many modern investment ecosystems (PE, VC, Hedge, ALT, SPAC, rollups) fracture before they root.

These are not short, nor designed for virality.

They are multi-sensory, slow experiences—built to last.

If this speaks to something you've always felt but rarely seen expressed,

perhaps these works belong in your world.

Both publication links are enclosed, should you choose to enter.

https://tinyurl.com/The-Silent-Treasury-1

https://tinyurl.com/The-Silent-Treasury-2

Warmly,

The Silent Treasury

Sanctuary for strategy, judgment, and elevated consciousness

Good read